US stocks surge higher, which is caused mainly by the better than expected ISM Manufacturing which came at 49.5 vs expected 48.5. Is the worst really over? The ISM infdex is still in a contractionary territory (for the fifth straight month). The outlook remains weak, partially due to the stronger USD but also weaker demand especially abroad but in general a secotr is affected by weak commodity prices, especially crude (affecting capital spending).

Source: Macrobond, XTB

Key bullets from the report:

ISM new orders index at 51.5 came unchanged, which is a positive signal, and as the gap between the new orders and inventory indices is a leading indicator for the headline, ISM index should rise slightly over 50 over next 1-2 months

The employment index rose rose to 48.5 in February, up from January’s 45.9 which was the weakest since 2009, we will have ISM non-manufacturing employment index on Thursday which will be far more important ahead of payrolls

Nordea points to a China’s Caixin PMI as a tentative leading indicator for ISM mfg and according to it ISM should not fall much further

Source: Nordea

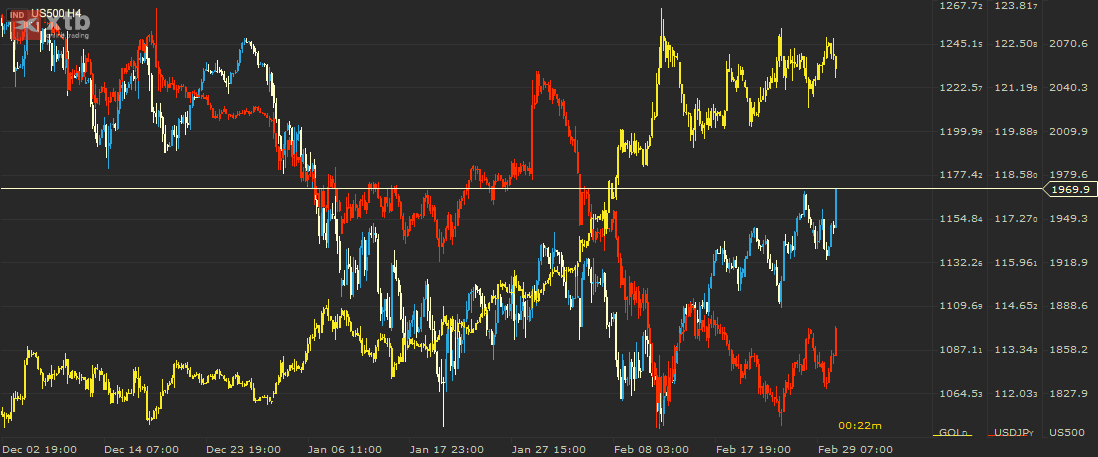

Stocks benefited from a better than expected report and moved distinctly higher. JPY deppreciates following risk-on attitude. A divergence between SPX and USDJPY has been partially closed.

S&P 500 comparing to Yellow Gold, Red USD/JPY

发表回复